Hey there, future financial whiz! If you’re tired of the stock market rollercoaster and looking for a way to add a bit of stability to your investment game, you might want to get acquainted with bonds. They might sound a bit stuffy or boring compared to the flashy world of stocks, but don’t be fooled—bonds can be a fantastic addition to your investment portfolio. Let’s break down what bonds are, how they work, and why you should seriously consider them. Grab a cup of coffee and let’s dive in!

What Are Bonds?

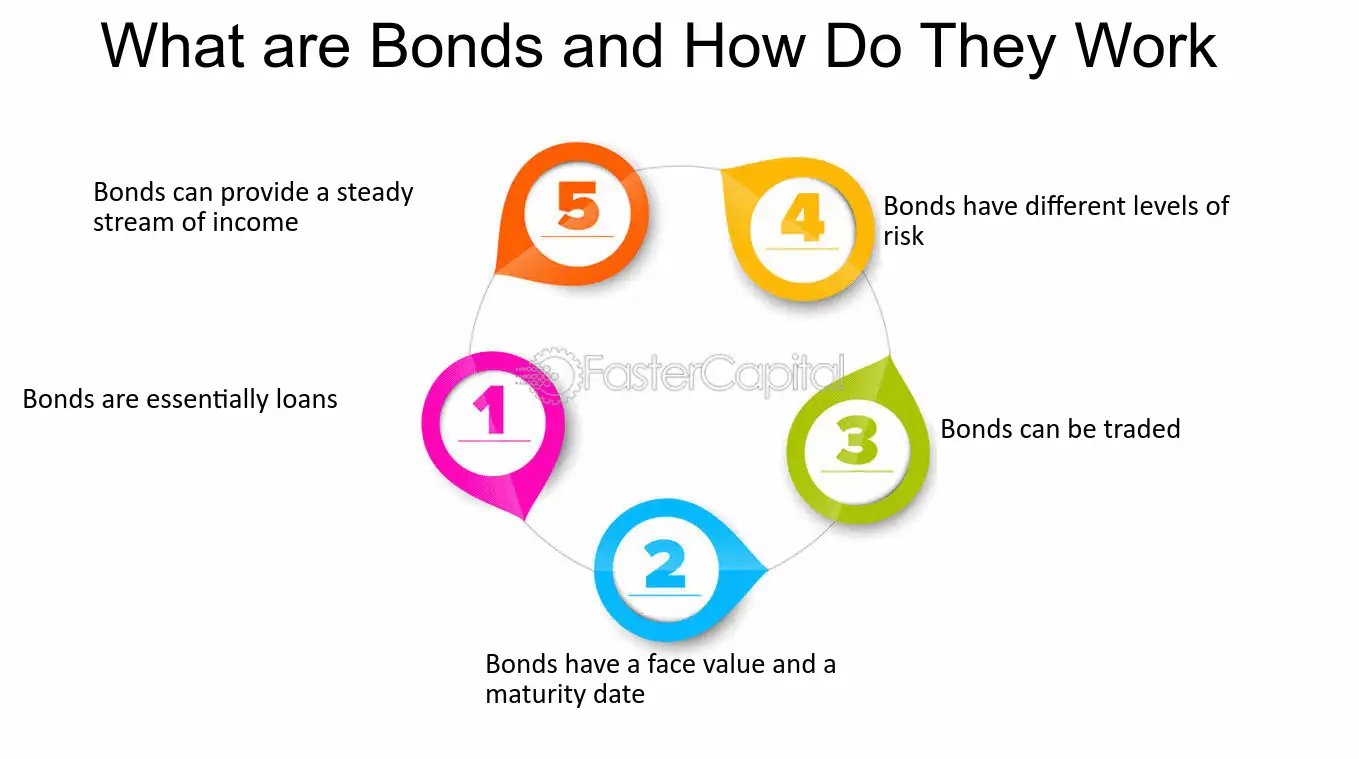

Imagine you’re lending money to a friend and they promise to pay you back with a little extra on top as a thank you. That’s essentially what a bond is—a loan you’re giving to a company or government, and in return, they pay you interest and give back your money on a set date.

Here’s a quick example: Let’s say you buy a $1,000 bond from the U.S. government with a 3% interest rate. Over the year, the government pays you $30 (3% of $1,000) in interest. At the end of the bond’s term, they give you back your $1,000. Not too shabby, right?

Types of Bonds

- Government Bonds

These are the safe bets of the bond world. Government bonds are issued by national governments and are considered super low-risk because, well, it’s the government. For instance, U.S. Treasury Bonds are like the security blanket of the investment world. In 2021, the 10-year Treasury bond had an average yield of around 1.5%, which might not sound thrilling, but it’s a safe place for your money to grow.

- Corporate Bonds

Now, if you’re feeling a bit more adventurous, corporate bonds might be your thing. These are issued by companies looking to raise cash. They offer higher returns than government bonds but come with a bit more risk. For example, Apple’s corporate bonds have been known to offer higher yields than government bonds. Just remember, higher yields often mean higher risks.

- Municipal Bonds

Here’s a feel-good investment for you. Municipal bonds are issued by local governments or municipalities to fund public projects like schools or bridges. They’re often exempt from federal taxes, and sometimes even state taxes if you live in the state where the bond is issued. For example, a bond issued to fund a new park in your city could not only help your community but also save you on taxes.

- Convertible Bonds

These are the chameleons of the bond world. Convertible bonds can be turned into a company’s stock if you choose. They offer the safety of bonds with the potential for equity upside. For instance, if you invested in a convertible bond from a tech startup, and the company booms, you could convert that bond into stock and benefit from the company’s success.

- Zero-Coupon Bonds

Imagine getting a coupon that doesn’t give you any money until the end but is sold at a discount. That’s essentially a zero-coupon bond. These bonds don’t pay periodic interest but are sold for less than their face value. For example, if you buy a zero-coupon bond for $800, and it matures in 10 years at $1,000, you’ll get the full $1,000 when it matures. The difference between the purchase price and the maturity value is your interest.

How Bonds Fit into Your Investment Portfolio

- Risk Management

Bonds are like the chill cousin of the stock market. They provide stability when stock prices are bouncing around like a trampoline. Diversifying with bonds can help cushion your portfolio from stock market volatility. For example, during the 2008 financial crisis, bonds generally performed better than stocks.

- Income Generation

If you’re looking for a steady stream of income, bonds are your friends. They pay regular interest, known as coupons, which can be a great way to supplement your income, especially during retirement. Just think of it as a paycheck you receive from your investments.

- Investment Strategies

There are strategies to make the most of your bond investments. One popular method is “laddering,” where you stagger the maturity dates of your bonds. This way, you have bonds maturing at regular intervals, giving you regular access to your money while taking advantage of interest rate changes.

Another strategy is the “barbell” approach, where you invest in both short-term and long-term bonds to balance risk and return.

Risks and Considerations

- Interest Rate Risk

Here’s the downside: if interest rates go up, the value of your existing bonds might go down because new bonds are issued with higher rates. For instance, if you’re holding a bond that pays 2% interest and new bonds come out offering 3%, your bond might not look so appealing.

- Credit Risk

If a company issuing a bond hits a rough patch, they might default on their payments. This is why it’s crucial to look at credit ratings before buying corporate or municipal bonds. Agencies like Moody’s and Standard & Poor’s provide these ratings to help you gauge the risk.

- Inflation Risk

Inflation can erode the purchasing power of your bond’s interest payments. If inflation rises faster than your bond’s yield, your returns might not stretch as far. For this reason, some bonds are designed to protect against inflation, like Treasury Inflation-Protected Securities (TIPS).

How to Invest in Bonds

- Direct Purchase

You can buy bonds directly from the government or corporations through various platforms. For government bonds, you can visit TreasuryDirect.gov. For corporate bonds, you might need to go through a broker.

- Bond Funds and ETFs

If buying individual bonds seems too complex, bond funds and ETFs are a great alternative. They pool together lots of bonds into one investment, giving you exposure to a diversified bond portfolio without having to pick and choose individual bonds.

- Choosing the Right Bonds

When picking bonds, consider your investment goals, risk tolerance, and time horizon. Are you looking for safety, or are you willing to take on more risk for higher returns? Do you need regular income, or are you investing for the long term? Visit official siteFinance phantom to get advice from investment experts.

Common Myths About Bonds

- Bonds Are Too Safe to Be Worthwhile

Sure, they’re safer than stocks, but that doesn’t mean they’re boring. Many bonds offer decent returns, especially when compared to savings accounts or CDs.

- Bonds Are Only for Conservative Investors

Bonds can be part of a balanced strategy for all types of investors. Whether you’re just starting out or nearing retirement, there’s a bond strategy that can fit your needs.

Conclusion

Bonds might not make your heart race like the stock market, but they offer stability, income, and a solid way to diversify your investment portfolio. They’re like the reliable friend who’s always there when you need them. So, if you’re looking to add a bit of security and steady returns to your investment mix, bonds are definitely worth a closer look. Dive into the world of bonds and discover how they can work for you. Happy investing!